What Have We Learned a Year After NASDAQ Hit 5,000?

January 21, 2002

Originally published on KurzweilAI.net January 21, 2002.

Although the Internet revolution is real and continues (e.g., continued exponential growth of e-commerce, the number of web hosts, the volume of Internet data, and many other measures of the power of the Internet), this does not change a fundamental requirement for business success: vertical market expertise. Most companies use the telephone, but we don’t define them as telephone-centric companies. Your local dry cleaner is likely to have a web site today, so the web has become about as ubiquitous as the phone, but we still want a cleaner that knows something about cleaning clothes.

The real Internet revolution has been the adoption of decentralized Internet-based communication by traditional companies to redefine their internal work flow processes and to communicate up and down the supply chain including end users. However, the proper definition of an Internet company is one that makes distinctive use of the power of the network. A company like eBay, for example, would not be possible in the brick and mortar world and makes unique use of its ability to match buyers and sellers.

We also learned that although a new technology may ultimately be destined to profoundly affect our civilization, there are nonetheless well-defined limits at specific points in time to its varied requirements. On the order of a trillion dollars of lost market capitalization in telecommunications resulted from absurd over investment in some aspects of the technology (e.g., the extreme glut of fiber) before other enabling technologies (e.g., the “last mile” of user connectivity) were ready.

Because of improvements in communication between buyers and sellers, this recession is not about excessive inventory. It resulted instead from a failure to develop realistic models of the pace at which new information-based technologies emerge.

It is also the case that the pendulum is swinging more quickly now, which reflects the overall acceleration of the flow of information. We went from almost anything goes a year ago to almost nothing goes four months ago to signs today of a renewed willingness to invest in new ideas by the angel, venture capital and IPO communities.

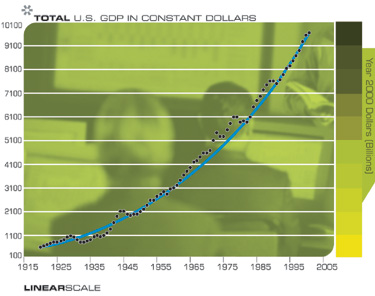

An important phenomenon I’ve noted from the recessions of the twentieth century (including the Great Depression) is that the recessions and recoveries reflect a relatively minor variability compared to the far more important trend of the underlying exponential growth of the economy. It is interesting to note that as each recession ended, the economy ended up exactly where it would have been (in terms of the underlying exponential growth) had the recession never occurred in the first place, as one can see in the following chart.

Chart Graphics by Brett Rampata/Digital Organism